The mortgage loan process brings together a wide range of professionals and a sequence of highly specialized tasks that depend on one another. With as many as 15 to 25 people touching a single file, even small missteps can slow progress. That’s why clarity around each participant’s role is essential, especially when it comes to two positions lenders often treat as interchangeable: the title agent and the settlement agent.

In many mortgage transactions, the same provider performs both functions, which is why the terms tend to get blurred. But these roles serve different purposes at different stages of the closing workflow. Understanding how they differ helps lenders make smarter partner choices, reduce risk, and deliver more predictable closings.

The role of the title agent

A title agent’s responsibility is to confirm ownership and identify issues that could jeopardize the transaction. This work begins with a thorough review of public records—deeds, liens, judgments, unpaid taxes, and easements—to ensure the property is free of outstanding claims. When problems do arise, the title agent works to resolve them by clearing liens, reconciling legal descriptions, coordinating with counties or attorneys, or working with underwriters to cure defects.

Once the research and remediation are complete, the title agent issues the title commitment and prepares the title insurance policies for both the buyer and the lender. Their role is fundamentally about risk management. The quality of this phase directly affects the ease and speed of everything that follows.

The role of the settlement agent

Where the title agent focuses on investigation and insurability, the settlement agent handles the operational side of bringing the transaction to completion. Acting as the central coordinator of closing, the settlement agent ensures the lender’s instructions, contract terms, and financial figures all align before documents are signed.

This includes reviewing the purchase contract or escrow instructions, setting up the escrow account, preparing the deed, settlement statement, tax forms, affidavits, payoff information, and the final Closing Disclosure. The settlement agent also manages all funds, receiving money from the buyer and lender, and disbursing payments to the seller, lienholders, tax authorities, and real estate agents. At closing, they oversee signing, confirm proper execution of documents, and record the deed and mortgage to formally transfer ownership.

In short, title establishes readiness; settlement ensures execution.

How the two function together

Although these roles often sit under one roof—especially in residential mortgage—they are not interchangeable. Title precedes settlement; settlement depends on title. In some markets, such as attorney states or escrow states, the roles may be handled by different entities entirely. And in certain transactions, including non-mortgage or personal-property closings, there may be no title insurance component at all, meaning only the settlement role exists.

This distinction matters in digital workflows as well. Modern eClosing and eNotarization platforms differentiate clearly between title, settlement, and notary functions because each requires different permissions, responsibilities, and system interactions. DocMagic’s ecosystem supports all three, which is why understanding the nuance between these roles is more important than it might have seemed during the paper era.

In a traditional paper closing, the handoff from title to settlement to notary happens almost invisibly because everyone is in the same room. In a digital environment, however, each of these roles carries distinct responsibilities that must be supported separately—especially the notary, who performs the final identity verification and document execution steps. This is why DocMagic’s environment differentiates between title work, settlement preparation, and the notarial act.

That complexity is something DocMagic accounts for intentionally when designing its eClosing technology.

“The closing has always been a complicated dance between lender, title, and settlement,” explains Eddie Oddo, DocMagic’s director of settlement and closing services. “Most eClosing vendors oversimplify what it takes to digitize the final signing event. Understanding every role in the process shapes how we design our technology. By giving everyone, from lender to borrower, the flexibility they need, our RON, IPEN, and hybrid eClosing solutions come together as the most complete and effective option in the industry.”

How this looks inside DocMagic’s technology

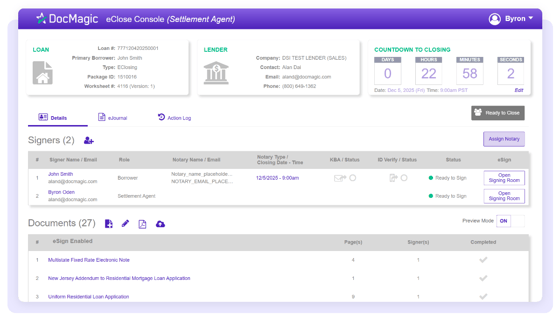

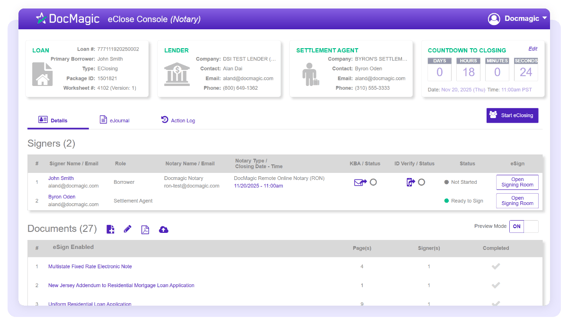

Because each closing role performs different tasks, DocMagic’s Total eClose™ platform presents a different experience for each user. For example, settlement agents see tools for preparing closing documents, balancing figures, and managing borrower appointments, while notaries see a console focused on identity verification, signing, and notarization steps. The screenshots below show how these role-specific workflows appear in DocMagic’s system.

[Figure 1. DocMagic eClosing console — settlement agent view]

[Figure 2. DocMagic eClosing console — notary view]

Value behind the scenes

Title and settlement work largely happens out of view, but lenders feel its impact immediately. Title agents spend hours resolving defects and safeguarding the transaction long before the borrower reaches the closing table. Settlement agents turn that cleared title into a complete, accurate, fully executed closing package. When each role performs with precision, lenders benefit from fewer surprises, cleaner files, and more predictable funding—all essential advantages in a market where data accuracy and efficiency define competitiveness.

As more of the industry moves toward fully digital workflows both in mortgage and in non-mortgage transactions such as eChattel and other personal-property closings, the foundational work done by title and settlement professionals remains central to delivering the kind of closing experience lenders expect and borrowers appreciate.

Topics from this blog: Industry Insight

BackSearch the Blog

- Recent

- Popular

- Topics

List By Topic

- Compliance (100)

- eClosing (85)

- Awards (74)

- eSign (71)

- Integrations (56)

- Industry Publications (52)

- Total eClose (44)

- eNotes (34)

- Remote Online Notarization (31)

- Document Generation (30)

- eDisclosures (25)

- eVault (19)

- GSEs (18)

- eNotary (17)

- SmartCLOSE (13)

- LoanMagic (12)

- eDelivery (11)

- Industry Insight (8)

- Partnerships (8)

- Philanthropy (8)

- AutoPrep (3)

Subscribe Here

Download the Truliant Federal Credit Union Case Study

Truliant took several key steps to refine its 100% digital eClosing process — including finding the right technology partner.